Process of Accounting

◼ Introduction:

Process of Accounting includes some steps that are followed to record transactions and get financial report of an organisation. Accounting is very essential part for every organisation. It is necessary to do accounting so that organisation’s growth can be traced.

As per the definition of accounting, it is a process of identifying, recording, classifying, summarising, interpreting and analysing all the monetary transactions and communicating the outcomes with the management so that better managerial decision can be taken for organisational growth.

So to do accounting work it is necessary to understand the process of accounting and steps included in it. In this article, we will learn from basics that how a accounting process start and where it is going to be end.

So Get Set Learn!

◼ Meaning of Transaction: Process of Accounting

The process of accounting starts when a transaction happens. Basically, when there is any exchange of things or any activity like purchasing, selling, paying, receiving payment, etc. happened then we can say that transaction has been done.

Transactions is of two types – Monetary Transactions and Non-monetary Transactions.

Monetary transactions are the transactions which includes flow of money. Like paying cash, selling goods, paying salary, receiving payment.

Non-monetary transactions are transactions which doesn’t include the flow of money. Like receiving gifts, taking chairs from home to office for office use, etc.

◼ Process of Accounting

The process of accounting is clearly written in the definition of accounting. Now we are going to learn all of them in detail. It is very important topic and very useful for beginners.

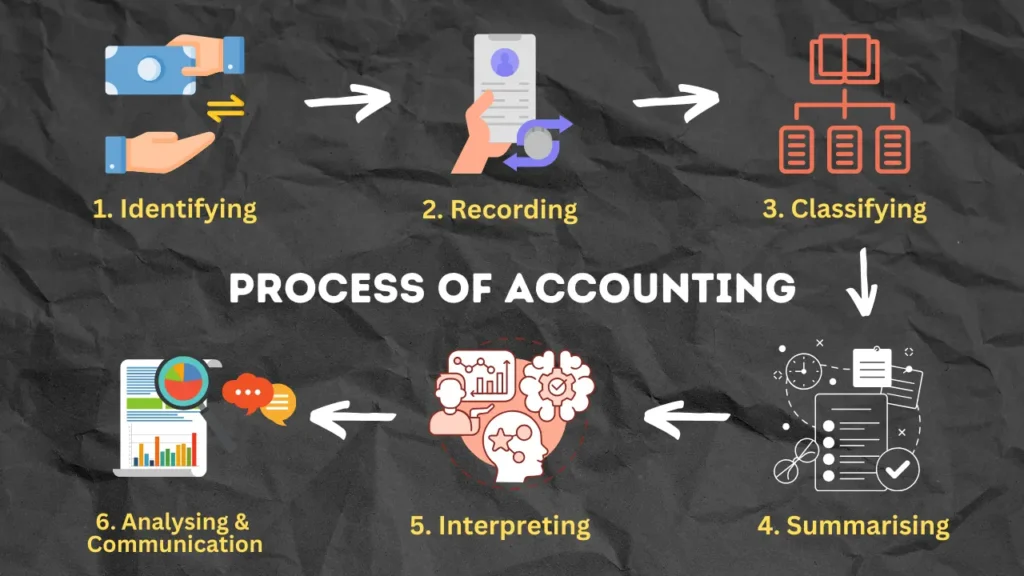

1. Identifying the Monetary Transactions:

In every business, lots of transactions are done on daily basis. They include both monetary and non-monetary transactions. First step of accounting process is to identify the monetary transactions.

As per the money measurement concept, accounting considers only those transactions whose value measurement can be done in terms of money. So the first step is to identify monetary transactions.

2. Recording the identified transactions:

After we identify the monetary transactions, then we have to record those transactions in our primary books. Such transactions are recorded in chronological order. Means the transaction that occurs first are recorded first. In accounting these transactions are recorded in two ways: either in journal or in the books of original entry (Purchase Book, Sales Book, Cash Book, Journal Proper, etc.)

3. Classifying the recorded transactions:

After recording so many transactions in the books, there would be mix up of each type of transactions. So the next step is to classify the transactions in different groups.

In this process, we categorise all the transactions by the name of different accounts and put the comman transaction into one group (account). We create a ledger book that includes different accounts and record all related transaction in it. In accounting, this process is known as ledger posting.

To read about Process of Accounting in short, check out our post on Instagram. Click Here

4. Summarising the classified transactions:

Classification makes it easy to look for different comman transactions in one place. But after classification there would be lots of accoumts with different balances. If we want to know what is the balance of any particular account, we have to search for that particular account in ledgerbook.

To overcome this problem, we have to go with the process of summarising. In this process, all the balances of different accounts are written on a single page. This would make it easy for us to see the total of every comman transaction on a single page. In this process we make Trial Balance.

5. Interpreting:

Every organisation always want to know whether it is making profit or not, what is it’s financial position, etc. Every organisation compares its results with its previous year report or with the report of its competitors.

For this, it is needed to prepare a statement of profit and loss and Balance Sheet. In this process we prepare Trading, Profit & Loss Account and Balance Sheet.

6. Analysing:

This step includes the comparision of current year data with previous year data, or with competitor’s data. This process includes horizontal analysis, vertical analysis, ratio analysis, etc.

7. Communicating with Management:

After completing all the steps and making the final accounts, the results are shared with the management. Management then takes decisions on the basis of the financial reports.

Also read our post on

Forms of Business Organisation

◼ Conclusion:

Accounting process includes various steps. Each step is important to complete the whole accounting process. It is necessary to obtain financial reports of organisations and for that process of accounting is mandetory to be followed.

1 thought on “Process of Accounting”